To Boldly Go: Why Frontier and Emerging Markets are worth exploring

In Short

AUTHOR:

Witold Bahrke, Senior Macro & Allocation Strategist at Global Evolution

Emerging Markets (EM) and Frontier Markets bonds stand poised to deliver substantial value for those ready to explore their full potential, says Witold Bahrke, Senior Macro & Allocation Strategist at Global Evolution, part of Generali Investments. In particular, frontier markets can offer a compelling role in fixed income portfolios, given their high yield potential combined with low duration.

Despite the challenges posed by weak global growth, global easing policies create fertile ground for positive EM and frontier market bond returns, which are expected to outperform developed market high yield bonds.

The combination of reduced macro-financial risk and improving growth-inflation points to better risk-reward profiles in EM bonds going forward, which can help offset slowing growth in China.

Frontier markets offer high yields with relatively low volatility, partly due to factors like lower duration and significant local investor bases, which helps to hedge against geopolitical as well as inflation risks, but also improves liquidity in periods of global financial stress.

The business cycle is bending, not breaking

Emerging market debt (EMD) is our exclusive focus at Global Evolution. Our investment approach is conviction-based and active. We invest only where we see potential, often taking substantial positions beyond the benchmark when confidence is high. We are pioneers in frontier market investing, where our unparalleled expertise, established since 2010, is extensive and nuanced.

Looking through the headline risks surrounding the US election, a number of key factors currently underpin a remarkably positive environment for EMD and frontier markets. Firstly, we think the economic cycle is bending, not breaking – while growth is cooling, we don't anticipate a recession in the next few quarters. The neutral rate, or the economy’s interest rate pain threshold, has risen, and the US labour market remains resilient, which reduces the likelihood of a major downturn. All being said, macro uncertainty remains high as inflation and geopolitical risks linger. Our scenario analysis points toward quite bifurcated outcomes. We therefore believe the real debate for 2025 is between reflation and recession, not goldilocks and recession.

For now, however, inflation has come off the boil, enabling EM and DM central banks to initiate broad rate cutting cycles. This transition from tight to more accommodating monetary policies is paving the way for favourable conditions in EMD. Despite the challenges posed by weak global growth outside of the US, these easing policies create fertile ground for positive EM bond returns, which are expected to outperform developed market (DM) high yield (HY) bonds. Currently, yields are particularly attractive, with EM hard currency (HC) bonds offering a yield-to-maturity (YTM) of 7.7%, providing a meaningful yield pickup relative to DM HY bonds.

Frontier markets present even higher yields, enhancing their appeal to yield-seeking investors. Frontier markets is a slightly misunderstood asset class; while high yielding, it’s often perceived as overly risky. We would counter that the actual numbers tell a different story: frontier markets serve as valuable diversifiers, offering downside protection in turbulent times without sacrificing much upside in favourable markets.

EM central banks have been ahead of the curve

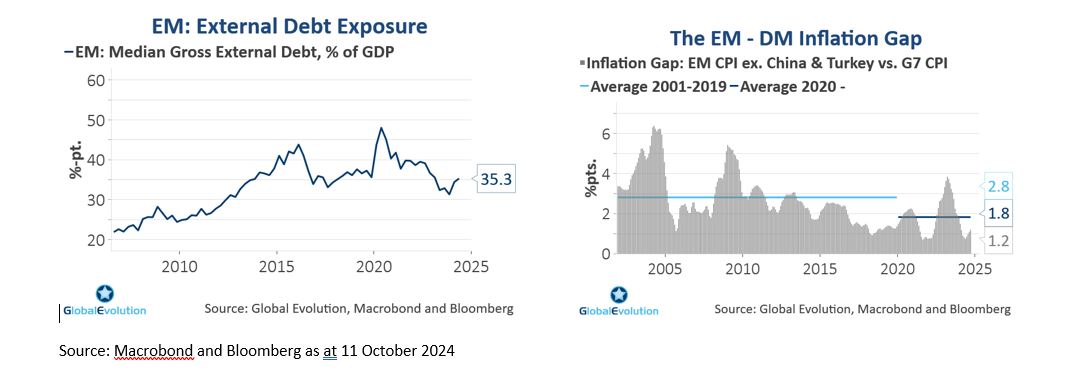

Looking longer term, the structural picture for emerging markets is encouraging. Overall, macroeconomic foundations are robust, and the growth-inflation trade-off is improving. External debt levels have declined lately, and current account balances have moved back into positive territory. Indeed, EM’s have increasingly avoided borrow externally in local currencies (see Figure 1). Moreover, leverage has only risen moderately outside of China.

Policy discipline in emerging markets has improved, with central banks generally ahead of the curve in managing inflation. This is in stark contrast to developed markets, which also saw fiscal balances deteriorate significantly more post-pandemic. The proactive monetary policy stance in EM has allowed inflation to return to pre-pandemic levels much faster than in DM (Figure 2). This combination of reduced macro-financial risk and a structurally improving growth-inflation picture points to better risk-reward profiles in EM bonds in the future. These dynamics are particularly important as they can offset the slowing growth trajectory in China.

Figure 1 and 2: Policy discipline is laying the groundwork for an improving growth/inflation trade-off in EM