Critical metals: learning from our material footprint

In Short

By Tarek Issaoui, Head of Macroeconomic Research at Sycomore Asset Management and Jean-Guillaume Péladan, Senior Advisor - Environment

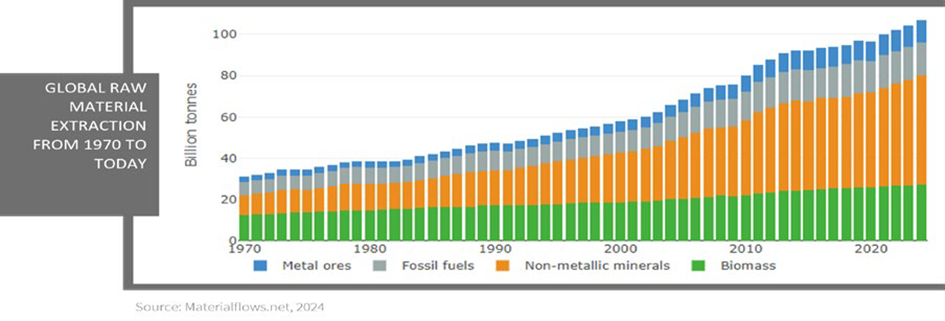

What material flows are needed to support human life? The concept of ‘material footprint’ attempts to answer this question. And the figures are staggering: our global material footprint has been growing by 235% since 19701. In 2023, 104 billion tonnes of abiotic and biotic materials were extracted, representing flows of 12.7 tonnes per capita per year. This is an average of 35 kg per day and per person throughout the world: 17 kg of non-metallic minerals, mainly sand2, 5.3 kg of fossil fuels, 3.4 kg of metal ores and 9 kg of biomass. 75% of these resources are non-renewable.

In rich countries such as France, the material footprint is far greater: between 18 and 29 tonnes of materials per person and per year, depending on sources3. In other words, on average, 50 to 80 kg of mineral, metallic, agricultural and energy raw materials – excluding water (or the figure would be much higher) are needed to support the lifestyle of a single person in a rich country4. We are unfamiliar with these orders of magnitude as we never actually witness the flows required for the extraction and production of the raw materials used to build our infrastructure, homes, equipment and support our daily consumption. “Out of sight, out of mind” and remote from our understanding of the world, to quote the late anthropologist Bruno Latour who pointed out the widening gap between the “world we live in” and the “world we live from”.

The facts are before us: the economic metabolism that sustains us is cumbersome and rather unknown. While materials supplying metals only account for 10% of mass material flows, they represent 17% of the weight of non-renewable abiotic flows and have a much higher financial value than non-metallic minerals (a kilo of sand is worth a few cents, a kilo of copper several euros, for example). In value terms, metals take the lion’s share! This also applies to energy consumption and to the many environmental impacts generated by the metals industry. The environmental and economic metabolism of metals is particularly heavy, thereby offering a perfect example of the ‘double materiality’ concept that is currently dividing the financial industry.

In this article, through an investment lens, we shall examine how this unheard of and physically unsustainable reality is already impacting – and will continue to impact - financial markets and investment strategies.

DEMAND ON THE RISE

As efforts are being made to transform our use of energy – with a strong focus on electrification, new types of demand are emerging and expanding. The global impact is all the stronger, as it comes on top of a power-hungry economic and industrial system set to last, and soaring demand for digital capacities.

The many studies conducted so far converge: the digitalisation of our economy and the transformation of our energy and mobility systems are aggravating factors, as they consistently require more infrastructure (servers, data centres, power grids, power generation facilities). Whether driven by generative artificial intelligence or electrification, this acceleration will only strengthen our need for metals. Historical observations have shown that the so-called ‘energy transition’ has, so far, involved superimposing and interlinking different energy sources and intertwining them with more and more materials - both in number and volume5. Most of these new needs require large initial investments in materials and energy.

Wind turbines, power grid components, electric vehicle charging stations and a fleet of electric cars? Their greenhouse gas emissions curves will evolve more or less in line with their costs: high at the beginning during the construction stage, then much lower during their lifespan.

Download the full publication:

1Global data from https://www.materialflows.net/global-trends-of-material-use/ and Écologie 360 n°3, p141-142, “Double vertigo” article, 2023. 26.25 tonnes per year per capita, PNUE, Sand and Sustainability Report 2022. 3 High income countries https://unstats.un.org/sdgs/report/2019/goal-12/ and France, cf. https://www.statistiques.developpement-durable.gouv.fr/sites/default/ files/2018-10/lps177-matieres-v2.pdf 4 Based on the average water footprint per capita in France :1,875 m3 per year, https://fr.wikipedia.org/wiki/Empreinte_eau, or 65 to 104 times higher! 5 Cf. “Sans transition”, by Jean-Baptiste Fressoz, Seuil, 2024

IMPORTANT INFORMATION

This article is prepared by Generali Investments based on information and opinions of Sycomore AM, relaying on sources both within and outside the Generali Group. While such information is believed to be reliable for the purposes hereof, no representation or warranty, express or implied, is made that such information or opinions are accurate or complete. The information, opinions, estimates and projections contained in this document are as of the date of this publication and represent only the judgment of Sycomore AM and are subject to change without notice. They should not be considered as a recommendation, explicit or implicit, regarding an investment strategy or advice. Before subscribing to any investment service offer, each potential client will receive all the documents provided for by the regulations in force from time to time, which the client is required to read carefully before making any investment decision. Sycomore AM may have made, and may in the future make, investment decisions for the portfolios it manages that are contrary to the views expressed here. Generali Investments and Sycomore AM assume no responsibility for any errors or omissions and shall not be liable for any damages or losses arising from the improper use of the information provided herein.

About Sycomore AM

Founded in 2001, Sycomore Asset Management is an asset manager specialised in listed investments and driven by a strong entrepreneurial spirit, part of Generali Investments’ platform of asset management firms. Since its creation, Sycomore has been committed to delivering long-term returns by identifying the levers enabling a company to generate sustainable value. The firm’s expertise draws on a fieldwork approach and a proprietary corporate fundamental analysis model, which includes financial and extra-financial criteria. Its investment team of 23 professionals focuses on assessing the overall performance of a company with respect to its stakeholders: shareholders, clients, employees, suppliers, civil society and the environment. Sycomore AM is a mission-driven company certified B CorpTM, thus marking its will to contribute positively to society: “a force for good”. Its mission: to invest to develop a more sustainable and inclusive economy for all our stakeholders.As a reference and key player in responsible investment, Sycomore AM is a member of the FIR, WDI (Workforce Disclosure Initiative) and IIGCC (Institutional Investors Group on Climate Change). It continues to work on the quantification of environmental and social impacts.

About Generali Investments

Generali Investments includes Generali Asset Management S.p.A. Società di gestione del risparmio, Infranity, Sycomore Asset Management, Aperture Investors LLC (including Aperture Investors UK Ltd), Plenisfer Invest-ments S.p.A. Società di gestione del risparmio, Lumyna Investments Limited, Sosteneo S.p.A. Società di gestione del risparmio, Generali Real Estate S.p.A. Società di gestione del risparmio, Conning* and among its subsidiaries Global Evolution Asset Management A/S - including Global Evolution USA, LLC and Global Evolution Fund Management Singapore Pte. Ltd - Octagon Credit Investors, LLC, Pearlmark Real Estate, LLC as well as Generali Investments CEE. *Includes Conning, Inc., Conning Asset Management Limited, Conning Asia Pacific Limited, Conning Investment Products, Inc., Goodwin Capital Advisers, Inc. (collectively, “Conning”). It is part of the Generali Group, which was established in 1831 in Trieste as Assicurazioni Generali Austro-Italiche and is one of the leaders in the insurance and asset management industries.

For more information: www.generali-investments.com